AAIR

-

Regarding the calculation of Actual Annual Interest Rate

Methodology

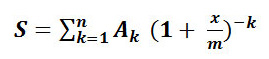

1. Mathematical methodology for calculation of Actual Annual Interest Rate (AAIR)

S —Net credit amount provided to the Borrower, i.e. difference between the credit provided and current deductions paid to Bank;

k-Raw number of money flaw (payment);

n-Number of money flaw (payments);

X-Actual annual interest rate ;

m-Annual payment interval

Ak-Sum of the money flaws (payments) on loan agreement. Bidirectional money flaws are entered to the account with opposite mathematical signs. In other words, money flaw which goes out are entered to the account with “minus” sign, and money flaw which enters into are entered with “plus” sign;

Note: Samples on calculation of AAIR based on this formula is provided at the end.2. The following payments should be considered during the calculation of AAIR:2.

2.1. The following payments in which the amount and payment period was clear during the conclusion of agreement:

2.1.1 Principal payments;

2.1.2 Interest on loans;

2.1.3 Commission charges on formalization of the loan agreement;

2.1.4 Costs on opening and implementing credit account, as well as costs on cashing the loan;

2.1.5 Costs on storage of collateral (mortgage) (if applicable);

2.1.6 Costs on assessment of the insurance and collateral specified in agreement (if applicable and if such services are carried out by the persons defined by the Bank);

2.1.7 Other administrative costs applied by the Bank on each individual loan.3. Payments not considered during the calculation of AAIR

3.1. Costs arising out of the requirements of country legislation, but not the terms of loan agreement, (for example, compulsory insurance, notary costs, etc.);

3.2. Costs arising out of the non-performance of the terms of loan agreement by the Borrower (for example, penalties for delay of penalties);

3.3. Payments, in which the amount or period of loan is dependent on the Borrower’s decision or behaviour and have been specified in agreement on performance of the loan (for example, commission charges on partly or fully payment of loan debt before the end of credit period);

3.4 Conversion on credit cards, stoppage of transaction and other such exemptions.